Argentina: Rising risk of government interference

Source: www.euromoneycountryrisk.com (scores inverted, 10=safest, 0=riskiest)

CLIQUE AQUI para ler o texto traduzido pelo Google Translate.

----------------------------------------------------------------------------------------------------------

Rising Argentine expropriation risk foretold by Euromoney Country Risk

Heightened risk of expropriation in the 12 months prior to YPF announcement revealed by indicator of analysts’ sentiment

In the comedy of economic errors that has blighted Argentina under president Cristina Fernández de Kirchner’s administration, Monday’s push to re-nationalize YPF, the country’s biggest oil company – expelling Spain’s Repsol as majority shareholder – represents one of the more dramatic shocks that has confronted foreign investors in recent years.

Understandably so. The prospective move harks back to Latin America’s penchant of yesteryear for asset expropriation and has triggered an ugly diplomatic spat between Spain and the commodity-rich economy.

|

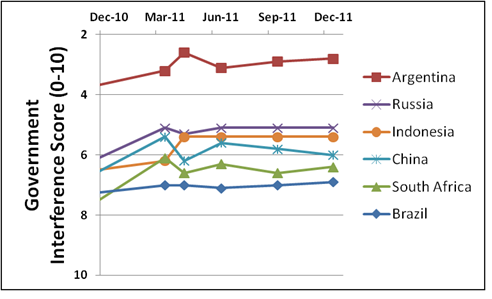

Argentina: Rising risk of government interference |

|

|

|

Source: www.euromoneycountryrisk.com (scores inverted, 10=safest, 0=riskiest)

|

But don’t say we did not warn you. Analysts participating in Euromoney Country Risk, which tracks economists’ perceptions of sovereign risk in 180 markets, have reported rising political risk in Argentina since the end of 2010, as the prospects for foreign capital have continued to darken.

A stronger warning was given by Argentina’s score in the survey’s indicator for government interference/non-repatriation of capital. Argentina’s score is the worst in Latin America, having fallen from four out of 10 in September 2010 to 2.6 out of 10 in April 2012. Prior to Monday’s announcement, Argentina’s government interference score had also been worryingly low in comparison with other emerging markets for many months.

|

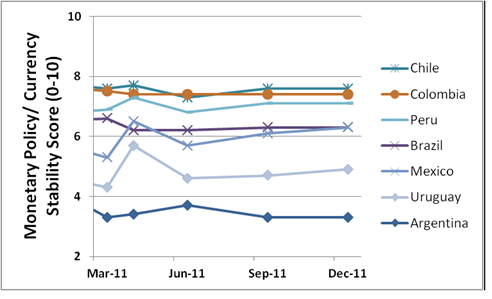

Argentina: Lack of confidence in the peso

|

|

Source: www.euromoneycountryrisk.com (10=safest, 0=riskiest) |

In recent years, Argentina has scrambled under Kirchner’s populist administration to boost money supply to increase investment and growth. The government recently removed legal limits to access on central bank financing to public and private sectors. It’s no surprise that these stubborn fiscal monetization efforts have resulted in a sharp fall in the peso and a rise in inflation – and a correspondingly low level of confidence in Argentina’s monetary policy among ECR economists:

Analysts’ views of Argentina’s financial position relative to Chile, the region’s poster-child for fiscal prudence, are negative. But Argentina’s scores are also poor in relation to other, less heralded Latin American sovereigns:

|

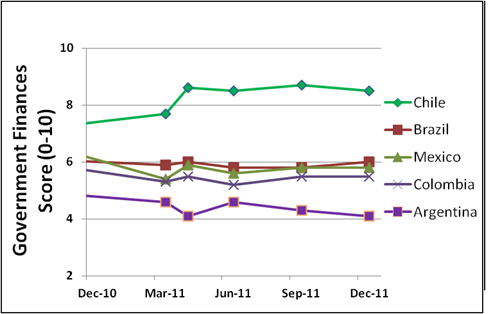

Argentina: Deteriorating Public Finances |

|

|

|

Source: www.euromoneycountryrisk.com (10=safest, 0=riskiest) |

After raiding domestic capital providers in Argentina – the social security system, state-owned banks and the central bank itself – the government is fast running out of financing options. If the government makes good on its nationalization push, then the prospect for foreign capital has darkened further.